Let's talk about why home prices are continuing to be so expensive. You want to purchase a home that's not going to drain your bank account, but the problem is home prices keep becoming further and further out of reach. And this has been an ongoing problem happening over the past few years.

But changes with COVID have made this even more apparent in our current economy as people are having to get on unemployment or potentially not being able to get unemployment yet and finding that. Rent and home prices continue to increase. So we're going to talk about three things.

Number one, why housing is so expensive. We need to understand the logistics that are going on behind here. So you can understand that it's not your fault. Also, we're going to talk about the areas with the most affordable housing and the most expensive housing. And then. How to keep your head above the water as these real estate prices continue to climb. So you don't feel overwhelmed the entire time.

My goal is to help you get your anxiety level from like a seven down to a four. So we can't take it away all the way. There's so many external factors, but the goal is to just alleviate some of this stress.

So first let's talk about why housing is so expensive. So in some of my discussions, I talk about how much a lender would give to you depending on your salary. So what normally happens is I get a comment on a video that says, maybe I make a video that says, if you make $50,000 per year, you can afford a $235,000 house. And then I get comments that say, where are you going to buy a $235,000? You're going to get a dump where I'm living at. And that's true in some areas, not all areas, but it's hinting at a larger problem that homes are becoming increasingly unaffordable and out of reach of the average person.

So I have some stats here that are pretty alarming and the goal here is just to help you understand that again, this is not your fault. This is an economic problem that's been growing for the past few years.

So average wage earners can't afford to buy a home in 344, 486 counties. That's 71% of the US that the average wage earner cannot afford to purchase a home, and without overextending themselves.

Also, median home prices have increased at four times the rate of household incomes since 1960. We can see since 1960, this is a 60 year old problem. Now that we're in 2020, it's a 60 year old problem. That homes are becoming increasingly expensive.

Also nationwide rents have increased at twice. The rate of household incomes since 1960, making, saving for a down payment difficult. So not only are home prices expensive, but rent is becoming expensive as well. And we're not seeing incomes rise at the same rate as a rents and home prices.

So it makes us really difficult as rent is becoming more and more expensive. It's not as much of a normal default option anymore to save money because rent is becoming so pricey.

The main cost are two things. Low inventory and low rates.

So low inventory. This is basic supply and demand. So when there's not a lot of supply left, that means there's high demand and high prices. So there just simply aren't a lot of homes available on the market for how many buyers are. There's a small pool of homes available in a large pool of buyers and low-interest rates are making it easier for people to afford a home, but the low inventory is pushing all the prices up.

So we have more buyers who are able to be qualified for these lower interest rate loans. And they're seeing these more attractive loans because of the low-interest rates, but there aren't a lot of homes available.

You might think where are all the builders at? Builders aren't building because, in 2008, a lot of builders went bankrupt. A lot of them don't exist anymore.

We're also seeing issues with building because land is becoming more expensive as well. And material costs is going up as well. So in some areas it's more expensive to build than to purchase an existing home. So we add all this together and we can see how overwhelming this whole thing really is becoming.

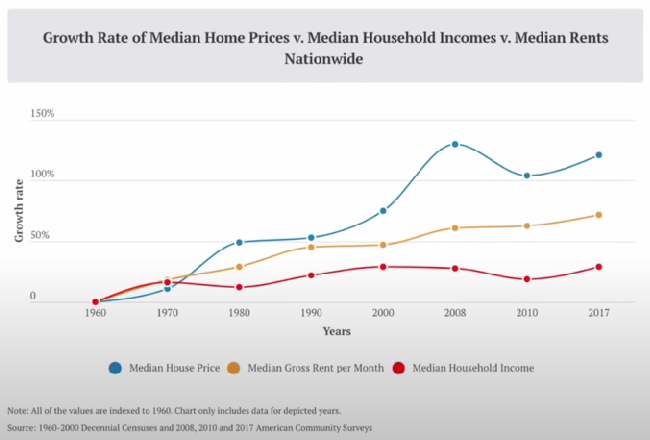

So two charts to look at that are pretty interesting. And this is telling of a, of what's happening in some of these statistics. So this red line is median household income. And we can see that since 1960, that increase has been about 40% up to 2017.

Now, if we look at home prices, median home prices, or the blue line. Since 1960, the increase has gone all the way up to almost 125% compared to the 40% of income. Now that's nationally, that's even worse if we look at just on the west of the United States. Again, about 40% in income and 200% and median home price.

So the west is becoming increasingly expensive, even more so than the US is nationally. Ideally, we would like to see income trending with home prices, right? As income increases, home prices increase. That's a level playing field, but what's happening is there's this disparity, this inequality happening where income is remaining static, and only the wealthier are able to afford homes.

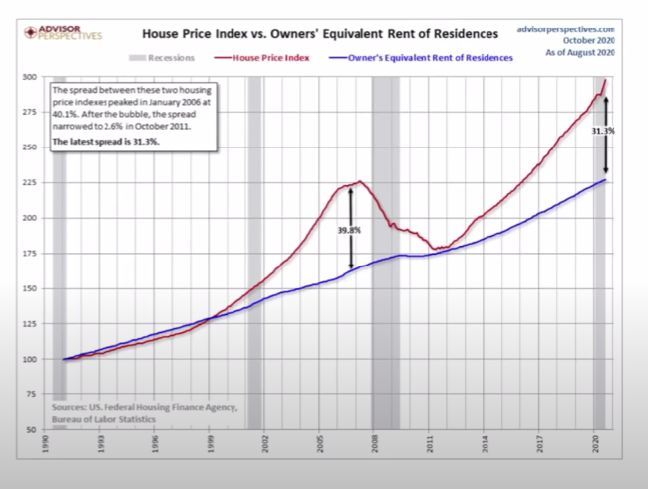

So something else that's interesting to look at is the difference between rent affordability and home price affordability. And we can see these spreads that begin to happen.

So the red line is the house pricing index. So think of it as the affordability relative affordability of a home. And the blue line is the relative affordability of rent. So as rent tends to stay consistent, compared to purchasing. We can see that what happened in 2008 is where we saw the housing crash happened marked by the gray line showing us the recession, but there was a 40% disparity in the affordability between purchasing and rent.

And we're seeing that happen once again, we had the housing crash happened here where everything declined and now these prices are rising again, and we're in the midst of this recession. So it's very possible that we're going to see this chart trail back down closer to the affordability of the renting.

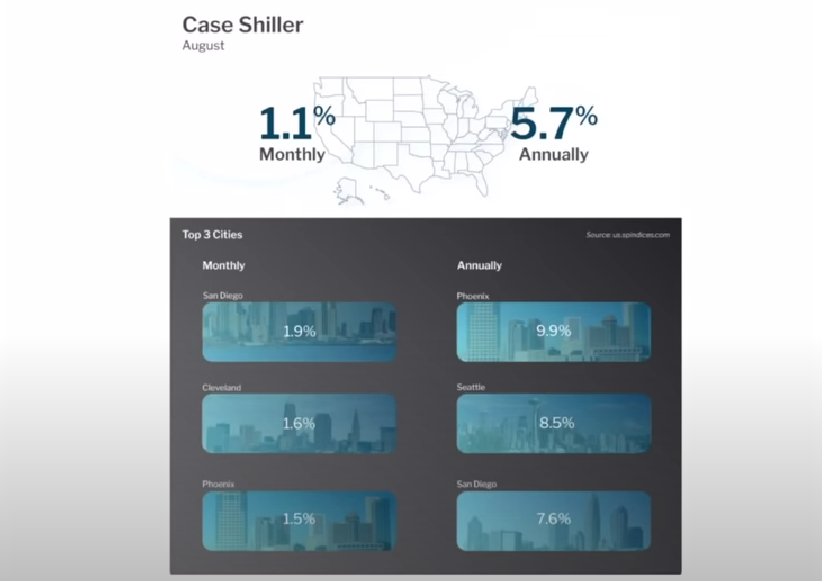

Also, we can see appreciation stats and some of these more expensive areas on how fast they're growing rate annually. We're seeing the affordability of homes. Increasing. So they're becoming more expensive by 9.9% and Phoenix by 8.5% in Seattle, and 7.6% in San Diego. And over here on the left, these are monthly stats, but annually and in the US we're seeing that appreciation grow by 5.7%.

So even amidst a job crisis in the midst of a pandemic homes are continuing to appreciate and become more and more expensive. And the question. When is this eventually going to slow it down? That's a great question that nobody really knows the answer to, but the point of this video is just to show you that it isn't your fault. Homes are expensive. I get it. And it's becoming more and more out of reach.

Before we dive into this, let's have a #CalmMoment. It can be really frustrating to see homes that are continuously growing in their value. And it feels like buying a home continues to be out of reach. Because ultimately you want a home that is not going to drain you of all the money that you have.

But the main problem here is that there aren't a lot of houses available and interest rates are low. So we have a lot of buyers and not a lot of sellers. So what can you do to maintain some calm in this frustrating and exhausting process when you're trying to get everything ready and do everything that you can, but home values, just continue to keep climbing.

Really the best thing that you can do is have patience. I know that's hard to do, but the best thing to do is to create a short-term plan. That's ultimately going to decide how you and your family handled the next three months, six months, and 12 months moving forward.

Because there are a lot of things that just frankly are out of your control, and the moment that we begin to realize that the things around us might not be within our control, we can actually have a little bit of relief because then what we get to say is what in front of us actually, do we have control over?

So things like what you spend your money on, how you save your money, and the way that you create and act with your money is really the only thing that you can control. You can't control house prices.

So the best thing that you can do is wait, have patients, and decide on a game plan. That's going to work for you in the short term. All right. I know it's frustrating. Sometimes we just have to sit back and accept that, Hey, the playing field might be a little unfair right now.

So the best thing that you can do is wait, have patience and decide a game plan. That's going to work for you in the short term. I know it's frustrating. Sometimes we just have to sit back and accept that, Hey, the playing field might be a little unfair right now. Instead of letting that beat you. Try to channel your energy into something that's more productive. So that eventually when the time is right, when the playing field shifts in the other direction, you now have the opportunity and the means to jump on that.

So now let's talk about the areas with the most affordable housing, because although those stats are really frustrating to see. So when we're looking at the areas with most affordable housing they're interesting to look at, and maybe it's worth considering if you're in a high cost area, the potential of moving somewhere else. And I know that can be a big decision and what a perfect world, and It'd be nice for where you're at if it's a high cost area for it to be a lower price.

The problem is most like the market's not just going to shift that way in your favor automatically, and home prices are going to be more affordable with where you're at. You might have to look at moving to a different location to find a more affordable housing.

Only 16 out of the hundred, most populated cities in the U S are below a 2.6 price to income ratio in 2019. So 2.6 is what a lot of economists call a healthy price-to-income ratio for people that basically means if you make a hundred thousand dollars per year, they would expect the price of the home of the average home for someone making a hundred thousand dollars a year is $260,000. That's what they consider as a healthy average.

Now in 2017, overall price-to-income ratio in the Midwest was 2.9%. So even above the healthy indicator, relative to a ratio, 4.2% average across the other three regions. So the Midwest is the most affordable place to purchase a home, but it's still above the healthy limit that a lot of economists would say that people should be taking on in the home price relative to their income.

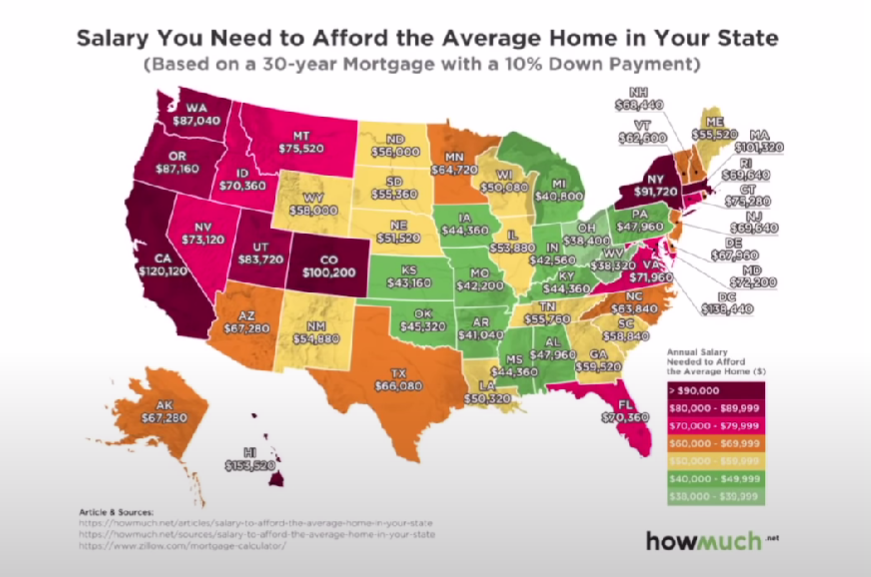

So we have the start showing us the average salary. You need to have to afford the average home in your state. And you can see, obviously, Midwest is your cheapest option here. When you start getting out west, this is where we see some of these highest costs becoming relevant, right? So New York is a little bit of an outlier over here on the right, but we can see Washington, Oregon, California, Colorado, and Utah these are all really expensive to live in. And Hawaii, always a little bit of an outlier too.

But you have states for instance, like Ohio, like I live in Ohio to purchase the average home in Ohio. You only need an income of $38,000. It's super cost-effective to live in Ohio or in other areas of the Midwest.

So it might be worth looking at if you are open to moving or looking at jobs or relocating, there might be worth looking at purchasing something more affordable. Especially if you live somewhere like Texas, maybe, is there potential that you can go to Oklahoma, Arkansas so you have a little bit more affordability.

So with that, let's jump into a quick break into ours. So the following is an advertisement from our sponsor Credible. So one of the simplest things you can do is shop for the lowest interest rate possible to save the most money when you get a mortgage. So credible is a marketplace where you can go sign up on their forum.

It's really quick, and they only do a soft credit poll. And what they'll do is they'll actually show you pre-qualified rates from different lenders. So you can see what's going to be the best loan option for you and your family moving forward. So it's simple. It takes only a few minutes to do something to know is credible does pay when the house you love an advertising fee.

If you do fill out a pre-qualification. So that is Credible Operations, Inc. NMLS 1681276. Not available in all states.

So we heard a lot of somewhat depressing information. So if you're stuck in this place where home is just out of reach right now, just know that's okay, but let's talk about how we keep our head above water. All right. Because if you're in the real estate world, a lot of people are just going to try to keep pushing you to, you need to buy, you need to buy, you need to buy.

But sometimes the best thing to do really is just to tread where you're at. That's perfectly fine. So what do we do in this situation?

The first thing that we need to keep in mind is that you don't want to overextend yourself just to keep up with other things. And I know it's super difficult with social media and seeing what other people are doing.

You're seeing people purchase homes and have new cars and families and new jobs. And normally what you're seeing online is not a true representation of what's going on. But don't feel like you have to keep up with other people and overextend yourself in the process. What you need to do is find the plan that works for you and find the thing that's gonna bring you contentment and joy.

And it's often, not keeping up with what other people are doing, even though it seems like that even though our mind wants to convince us that's the truth.

So budgeting is key. If you don't have a system to budget right now, then you're never going to get farther than this feeling of being overwhelmed and frustrated by the home buying process. And what I mean by budgeting is not just having a general idea of how much you spend. That's an expense report. A budget is actually something that you consult every time you make a purchase to see. Do I actually have the money for this, or is my money needing to be used on other important things?

There are two pieces of software that I really like for budgeting one is called YNAB or You Need a Budget and the other is called EveryDollar. These are two great budgeting software. They're going to help you figure out what your budget looks like. So you can see where your money's actually going and how you can readjust it in the future. That way you can explore creating savings, paying off debt, saving for a down payment, and how much you could afford with a future home.

Now, what I first want you to do is realize that just because you can't afford a home right now, doesn't mean you have to give up on all the other financial areas of your life. You don't want to just say I can't afford a home, I'll throw in the towel.

When you first want to do is see what are ways that you can get small wins right now that are eventually going to build up into these bigger wins, that help you eventually purchase a home. And the first thing that you can do is pay off high-interest debt. So for instance, credit card debt. If you have credit card debt, let's quit and take care of that. That's way more important than purchasing a home right now.

So look at paying off high-interest debt and building savings. Again, you'll never be able to do this unless you have an effective budgeting system. That's going to keep you on pace and on track for your goals moving forward. You can't even create those goals unless you have a budget in the first place.

Now, if you do get to the point where you're ready to purchase a home, You need to make sure that your mortgage payment is affordable. And a lot of people ask what's a good way to determine affordability.

A good rule of thumb is to take your net income, so your take-home pay and don't let your mortgage payment be more than 25% of that amount. So your principal interest taxes, insurance, and HOA fees need to be less than 25% of your income. That's going to make sure that you're not overextending yourself on purchasing.

Then finally, if you have the patients wait out for a price correction, we, if we go back to that chart that we saw that pre. We saw the home price index skyrocketing above rent and then came tumbling down. Now that was because we had a bigger economic problem underlying, but we're most likely going to see an additional correction.

I don't think we'll see a crash because we have a solid economy, more solid than we did pre-2008. But we're most likely going to see a price correction. That means prices are going to go down. So if you have the patients weigh that out and you most likely see home affordability become lower to the point where it's a little bit more in reach and under grasp for you.

But if you don't have these initial, this initial framework, this initial foundation set up like budgeting, savings, and paying off high-interest debt. Then even if we get a price correction, you might not be ready for it. So make sure you do all those things first before you start looking at purchasing a home.

Ask us a question →

Ask us a question →