Interest rates now are getting close to 5% and as home values continue to go up as well as interest rates go up, it starts to ask the, we start to ask the question, can I actually continue to afford a home? Or is this going to push me out of being able to afford a home either right now or in the future?

In this blog, I want to give you a game plan to help you understand if you can still afford a home with interest rates continuing to go up and a way to make sure that we don't make decisions based on panic. When things like this change, when our external circumstances change, it can be really easy for us to get into panic and not make a really good decision about what we're going to continue to do moving forward.

First of all, just want to talk about what interest rates are where they're at today. So you can go to WTHYL to see an average of different loans and the rates. So right now for a 30-year conventional, it's at 4.811%. If we take a look at the trend of rates, obviously over the past month, they've been increasing quite a bit going from 3.98 now up to 4.8. If you check out my website, WTHYL, you'll be seeing that huge almost one-point increase over the past month. And we went from what was super historical, low-interest rates to now things increasing.

What ends up happening is it pushes us into this fear of, oh my gosh, I have to either buy now or I have to completely ditch home buying and want to help you make a more clear decision about how you can move forward.

You will also see the other rates for things like jumbo loans, FHA loans, and pretty much everything has increased over the past month. Now really what I want to help you understand is that just because things change externally this shouldn't be a threat to your ability to own a home because we have to consider so many other things when we're looking at buying than just the interest rate that shouldn't dissuade us from all of the other reasons why we might want to buy a home.

And what I think this situation forces us to do is really to reacclimate with the numbers, and that's rerunning the numbers. So for instance remember when you've ever like a, bought a fish, it came in that little bag and it's like jostling on the way home in the car. And you have to put that bag into the fish tank to let the water even out. I don't know, fish terms but the fish has to re-acclimate to the water around it and its temperature. We have to do the same thing with this home buying market, as things are changing so much, what's ending up happening is we're getting stuck in just looking at the numbers and what they use to be. And think that's what should happen going forward.

The interest rates used to be super low and that's the way they should always be. And if they aren't, then we're going to panic and act like we can't do anything. When in reality, if we can take a moment to reacclimate to what the market actually is and accept this is what's going on, there's nothing that we can do, no one can do anything to change home prices, changing to change interest rates changing. The only thing we can do is accept what is actually happening right now.

And so there's this phase of re-acclimation that I think we need to go into and, keep in mind like I'm not just pushing this because I want you to buy a house like this isn't a topic just centered around like everyone should buy and buy. I'm buying a house this year too, or at least that's my plan. And I'm running into the same problem that you are, I'm sitting here, I'm not going to be ready to buy until somewhere around mid-June or after that. And I just have to keep seeing home values, continue to increase and interest rates continue to increase. I don't like that either.

But at the same time, I'm continuing with my plan to move forward with buying because buying to me is more about just the interest rate. It's more than just the interest rates, more than just what the price of the home is. Buying a home to me means a lot more things than just those two numbers.

What's been really helpful for me is that since I see numbers for buying a house almost all day about interest rates, closing costs, down payment, values, and everything like that is that I get to get reacclimated to that very often. So you might need to do the same thing. Maybe the numbers that you've been running in your head were numbers that were from last year. And then all of a sudden you saw this year's numbers and it's a little bit of sticker shock. It was a big increase.

What I think is really helpful is to start rerunning these numbers, to make sure that through the process you're reacclimated to if interest rates increase, what are those numbers? Now I can make a decision based on what the actual data is with the actual situation is not just based off of well, if I bought a year ago, it would have been a hundred dollars, $200, $300 a month cheaper. Maybe, but that's not reality at the moment.

So what we need to do then is figure out what are these numbers again. So a really great action step for you to take would be to talk with your loan officer and get an updated payment that is at the current market. See, if you can talk to your loan officer and say, Hey, I know we saw what the payment would look like at interest rates a week ago, but could you give us an update on with the monthly payment would look like now and potentially what the monthly payment would look like if interest rates continue to increase in the next month or two months.

That way you can start getting a really realistic idea of what are these numbers. Because I think in our head, a lot of times we can see, okay, interest rates increase. And in our mind that payment is skyrocketing. When in reality, that might not be the case. And when you're making a decision as big as the security, safety, and freedom of owning a home for you and your family, when you're making such a big decision that you don't want it to be based on a number that isn't actually driving a lot of the decision for you.

So I want to show you a couple of calculations here using this tool that I call the LoanClarity Advisor you can take a look at it. What it does is it helps compare loans and different scenarios. So you can see really what is going to be the best option for you moving forward.

First going to start with the scenario, the median home price right now in the US is around $410,000. So we're going to use that, and I'm just going use some estimates for the state of Ohio since that's where I am at. So let's first look at one loan. Today's rates. So we're going to a conventional loan with 5% down for 30 years. And let's say we're looking at a 4.875% interest rate right now. It's 4.811, but we're going to round up to 4.875 since usually interest rates are given in eighths of a percentage bracket.

So let's look at today's rates. Let's also look at what future rates might look like. Same thing, conventional 5% down,30 years. Let's say interest rates went up to 5.25% and then let's take a third option. Let's take a look at what rates were. All right, 4.25 so all of these loans are the exact same. They just have different interest rates.

Now that we have all of the information, let's scroll down and take a look at what are the costs of these loans. So let's say we're looking at staying in the home for 10 years. You save $40,000 by having the past rate option. However, this is one of those things where we look at it and we're like, man, I would've saved so much money. And somehow this dissuades us from wanting to purchase in the future, and we're like, oh man I made a mistake and I didn't buy them. And so I'm not going to buy at all.

And the problem is that's just not reality. We can't access those pass rates. Maybe they'll lower in the future and we'll be able to get access to them, but we don't have them right now. So let's actually take this out of the mix and just look at these two.

Obviously, today's rates are going to save us a lot more money than the higher interest rate, but when people are talking about the benefit of owning a home. It's not that a home is this crazy great investment. Sometimes it can be, but really the main bit of benefit of buying is the fact that it's a much better option than renting.

Don't think of your home as this incredible investment opportunity or investment vehicle. The best thing about home buying is the fact that it's a much better option than renting. And that's really what we're wanting to compare it to. So if we took both of these loans, and let's say we looked over 10 years, a historic appreciation over the past 30 years is 4%. And let's say it costs us 6% to sell with the fees to sell and realtor commission.

What would owning a home cost us or benefit us? So even though these rates are higher than they were in the past, with today's rates, It would have cost us $33,000 over 10 years to own a home with this loan. If rates increased, it costs us $48,000 over 10 years. And we're factoring in appreciation minus the cost to sell minus the cost of these loans.

So even though these were much more expensive loans than if we got a 4.2, 5% rate. It only costs us $33,000, $48,000 over 10 years. Now, I think sometimes we can look at this and think everyone's actually told me buying a home is beneficial. I'm going to make money if I own a home. And sometimes that's true, but it's not always true.

Again, keep in mind that owning a home's main benefit is that it's better than renting. Not necessarily that it's some insane lucrative investment opportunity for you. Because if we compare this to renting for comparison, a rental payment of let's say we have a rental payment of $1,600 per month and an annual increase of 3% per year, which is the national average rental increase that would cost you $220,000 over 10 years.

So if you are checking the graph on my website, even with today's rates, even though they're much more expensive than they were, let's say when it was 4.25, or when it was 2.5, even though we're at a 4.75% interest rate right now, or a 4.875, it only costs us 33,000 compared to $220,000. Even if we compare this, let's say $1,200 per month in rent.

It would have cost us $165,000 over 10 years to rent versus only costing you $33,000 over 10 years. Or if interest rates increase only $48,000 over 10 years now let's make this slightly more realistic. Let's say we're also paying, it didn't include closing costs, in the beginning, let's say there's $10,000, and closing costs are a really rough estimate. So if we do that, it costs this $43,000 compared to, again, $165,000.

Are there any costs for maintenance? Did you have to repair the roof? Did you have to make upgrades? Did the furnace go out? Okay. Will you still have $140,000 worth of work you can do over the next 10 years? I doubt you're gonna put $140,000 worth of work into your home. As long as you're below that. Buying is still a better option than renting.

I think that's really important to keep in mind is the fact that even if interest rates do increase to 5.25%, the cost is 58,000 compared to $165,000, rent would have to be extremely low for it to be a better option, even if rent, even if it is 450 a month, buying is still a better option in this scenario. Even if rates go to 5.25%, right? And if you have a $450 a month rental payment, please let everyone know where you live. And hopefully, there's no way that would be a nice place to live in. Maybe if you have rent that's that cheap and it's a great place, please let us know where that's at.

So I think it's important to keep in mind as we're looking at things happening because the interest rates go up and it's really easy to panic and says, everything's falling apart. There's no way I'm going to be able to afford to buy a home. But, it's the opportunity cost of missing out on being able to buy a home and saving so much money compared to renting, and don't get me wrong. I do understand that it is getting more and more difficult to get approved for a loan. And I don't want to minimize that at all, but what I want to help illustrate is if you can get approved for a loan. You really do spend so much more by renting than by owning a home.

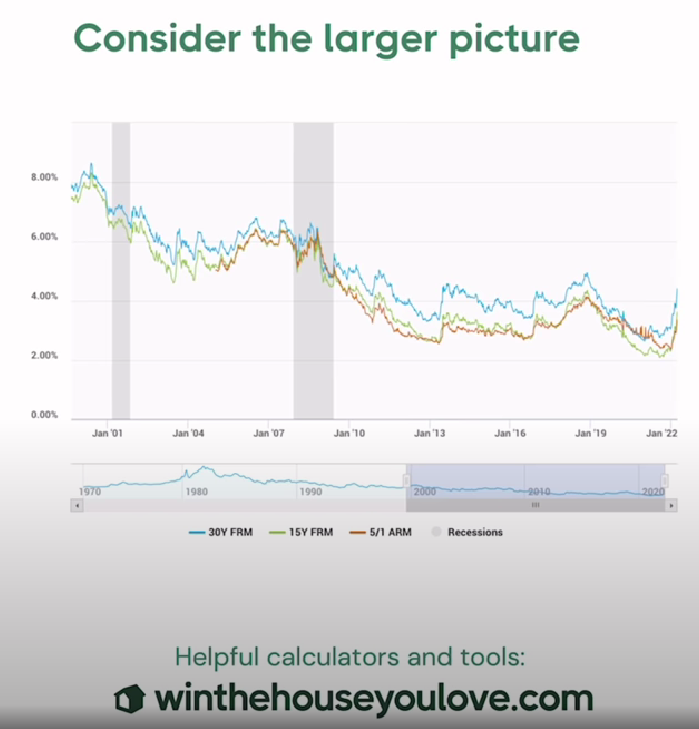

If we look at historical information, the interest rates here just before April of 2019 interest rates were at the same point that they are right now, tracking along with interest rates today. What ended up happening is that plenty of people bought here in 2019. Then when interest rates dropped down, getting closer to a sub-three interest rate range, people refinanced. Interest rates went up and then if there is a future potential for interest rates to go down, there is also a refinance potential as well. So if interest rates go down in the future, you can refinance.

And on the flip side, interest rates may not go down. No one can predict the future of what's going to happen. And if interest rates continue to go up, just like in the previous example, even if they're at 5.25, that's still a much better option than renting. Also, we could probably take the interest up to a crazy amount and it's still going to be a better option than renting for most people.

Then, if we consider the larger picture. Because what happens when you get into the home buying world is that you're really only paying attention to what's happening in the home buying market for as long as you're in it. So maybe you only started considering looking at buying a house four months ago, and you've really only been paying attention to what's been happening with home values and interest rates and the housing market for the past four months. So we have this really narrow view when we really need to consider the whole picture.

If we track the graph line straight back, we can see that it's actually on track with half of this historic data for the past 10 years. Then we have a ten-year period for that. That was on average higher. So we take a look, at this historic range, is this increase happening? Absolutely. Is it on track with the past 10 years? Yes. Is it better than the 10 years before that? Yes.

Again, I don't want to minimize the fact that home buying is getting more difficult. Home prices are increasing, which means the monthly payments increasing along with the interest rate which doesn't help their monthly payment either. And the down payment is increasing as home values increase as well. And so I totally get it. It is getting more difficult to qualify for a loan, more difficult to put in an offer, and more difficult to find a home that is affordable. But at the same time, it's not diminishing. The fact that home buying is still a really great option compared to renting, even as home values continue to go up.

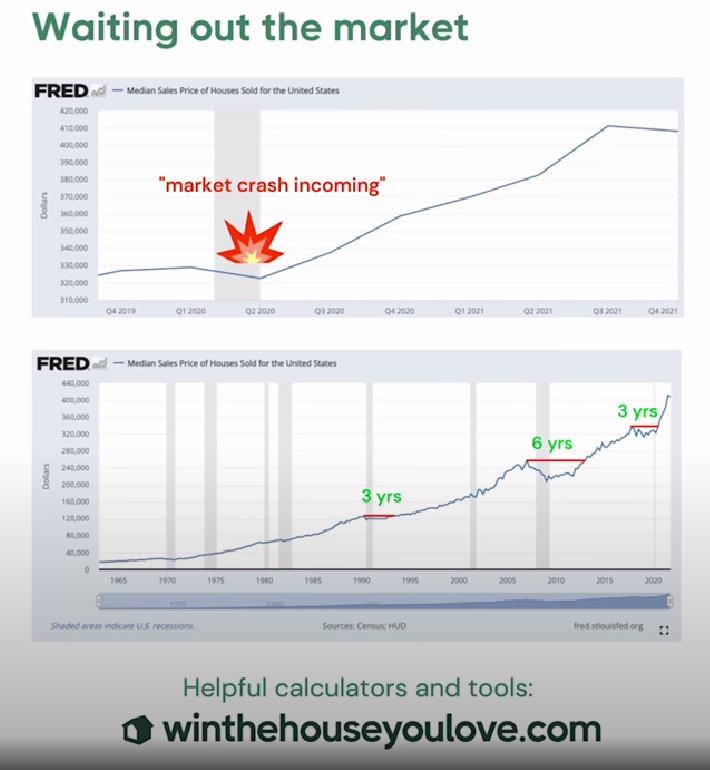

So this usually brings up the question of, should I, or should I wait out? When home values increase and interest rates increase. A lot of people say, okay I'm gonna sit back and wait this out and hope that things go down, and then I can buy when things get lower.

This is what happened a lot at the beginning of 2020, right around the 2nd quarter is when a lot of people were saying, there's going to be this huge market crash coming, and so far it's been the opposite. As home values have continued to go up. Even though all the alarm bells are, people were ringing at the beginning of 2020, instill are doing them everywhere, and I'm not naïve. No one knows what the future is going to look like. Home values could drop.

I don't see the data to support that, but it's something that could happen. And certainly, we're not making our guesses just off of well if one chart goes up, it all goes up. But if we look back at the historical data to inform us of what could happen in the future, what we end up seeing is a chart that looks like what's happening a year or the past two years from 2020 to 2022. There was a 23.7% increase in home value. If you bought a home at the beginning of 2020, and let's say you put 3% down in two years, PMI would be off of your loan. You'd have over 20% equity in your home. That certainly is not the market crash territory.

Then if we look at an even scaled out view from 1965 to 2021, we can see what home values have done. There's only been three major instances where home values have dipped. This happened in the beginning of 2015, or a closer 2016. Also with the 2008 housing crash, and then here around 1990. And in each of these instances, the most it took for someone to recover their money was six years.

So for instance, there was a drop in home values. If you bought at the height of that market at that little bubble, home values then decreased. As long as you were in your home for three years, you would have broken even on the value of.

Same thing in 2008. We hear about 2008, and I think there's this fear of, "what if that another one of those happens?" and don't know be wrong. A lot of people lost their jobs. A lot of people lost tons of money, but if we're taking a very safe approach with the way that you're buying and making sure that you're not stretching yourself too much, and you do have cash reserves to be able to weather some downturn.

Even if you bought at the height of home values increasing, or even though values dropped down. If you were in your home for six years, you didn't lose any money. And the average person is in their home for 10 years. Same thing with other small drops that we had. If you bought at the height and then it dropped as long as you were in your home for three years, you didn't lose money. And in fact, the people who bought at the height, if they kept it for 10 years, they would've made money. That's the average time that somebody is in a home.

So if you are choosing to wait out the market, then the question is, are you smart enough to be able to perfectly time the dip? Because you would make more money if you bought in early 2005 and then could sell around 2015 which is higher. Absolutely. But there's no one that I know of that is able to time the market that no one really has a crystal ball that can do that. Now again, I'm not naïve in thinking that just because this chart goes up, it all goes up forever.

I think values are going to stabilize over the next couple of years. I think we're still going to see appreciation still going to see values increase. Hopefully not at the pace that they are over the past couple of years, but it's important to have this historical perspective here in realizing that even this huge crash that happened in 2008, as long as you stayed in your home for six years, then you didn't lose money by owning your home.

So ultimately what I want you to take away from this is the idea that a calm game plan is way better than that panic that is going to shift your timeline. Remember why you're buying a home. It's not just because the interest rate was low. I'm hoping you're not buying a home just because you saw a low-interest rate. That's not a very good reason to buy a home. It's a good reason to buy an investment, not a great reason to buy a home that you're going to live in.

So what I want you to do is to rerun your numbers and get reacclimated to where we're at. It's fun to play the what-if game of what if I bought when interest rates were 2.5%? Why wouldn't that be great? Yeah, but that's not the present. That's not reality. And it doesn't do anything to help us move forward with the goals that we have. So we need to rerun the numbers and get acclimated.

So if your timeline is saying, I want to move out of the house I'm in because it's cramped because I don't like where I live because it doesn't feel safe because it isn't a part of my family goals for growing my family.

If that is what your timeline is, and that's what you want. Your actions should fall along with that. And not be well, the interest rates went up another quarter percent, so I'm fine with living in a home that doesn't align with what I want in the future. That is starting to make sense.

Also, consider why you want to buy. Is it security? Is it stability? Is it freedom? Is it something else? There's been this weird narrative in real estate? I think is really just marketing. The thing that people do, where they try to convince you that buying a home is supposed to be an investment, and the home does appreciate in value historically. We saw that and sometimes at home can be a way to make money. Some people make a lot of money by living at home and it increases in value and the time the market just right, where they made a lot of money.

Buying a home really in my opinion is not a great investment option. The reason it says it's a better cost-saving option or kind of pseudo investment is that it's a much better option than renting.

The alternative or renting is a terrible option compared to the cost savings that you get from owning a home, and keep in mind when I say renting is a terrible option, I only mean from a financial perspective, renting still gives you tons of freedom of location. You can move a lot. It's a lot more flexible. There are so many things that you can do with renting. That's much better if you're staying in a home or staying in an area for a shorter timeframe. But It costs so much more than owning a home.

A home is a primary vehicle of safety and freedom and investment is something that trades risk for a reward. So don't confuse the two. Don't muddy the waters by forcing your primary residence the place that you're going to call home to be both a home and an investment.

So ultimately you have to make a decision, can you still buy a home with a 5% interest rate? The best thing to do is to rerun those numbers and figure out what's going to be the best option for you. Moving forward. Look at historical data and see if this is still an option that's going to work well for you.

Ask us a question →

Ask us a question →